The 3rd way of credit

in Brazil.

PraQuitar enables the full settlement of debts while creating new performing financial assets from origination.

We are a new infrastructure that complements the credit market — the creditor receives an upfront payment, the debtor pays in installments, and the system becomes more efficient. Settlement is a natural evolution of the credit and collections market.

The challenge of delinquent credit in Brazil

Traditional collections

The current system offers installment plans that do not fit the debtor's budget, often leading to broken agreements and renewed negative credit reporting.

Sale as NPL

Deep discounts and value destruction. The creditor accepts a fraction of the original amount to remove the problem from its balance sheet.

We created a complementary model that strengthens the credit ecosystem.

The failure is not the debtor. It is the infrastructure.

Most debtors want to repay their debts. The problem is that they lack the liquidity to take advantage of the best terms: full upfront settlement.

"The system never created a mechanism connecting the willingness to pay with the ability to settle."

Lack of immediate liquidity

The debtor lacks the capital to settle upfront, even when a discount is available.

No discounted installment option

The system offers either an upfront discount or installments with high interest.

Lengthy, exhausting processes

Endless negotiations that frustrate both sides.

The credit market only sees your past.

We believe in your fresh start.

When no one is willing to extend credit, the system closes its doors and opportunities disappear.

But what if there were another chance?

PraQuitar was created to enable fresh starts. We lend without focusing on past credit scores; instead, we look toward a future with restored credit standing.

The market had two options. Now it has three.

Upfront discount

The debtor lacks the liquidity to take advantage of it.

Traditional installments

Unaffordable payments lead to one outcome: a broken agreement.

PraQuitar

We settle upfront and finance the settlement in installments.

PraQuitar is a new infrastructure that complements the credit market.

We settle the past and originate a new asset, strengthening the credit ecosystem.

It is not renegotiation. It is origination.

PraQuitar does not recover debt. It creates a new financial asset.

Immediate settlement for the creditor

The creditor receives an upfront payment. The problem is resolved immediately.

A new agreement with the debtor

A new obligation is created — structured, predictable, and free from the burden of the past.

Performing asset from day one

The new agreement starts as a healthy, performing financial asset.

The problem ceases to exist. A new asset comes into existence.

The point where value still exists

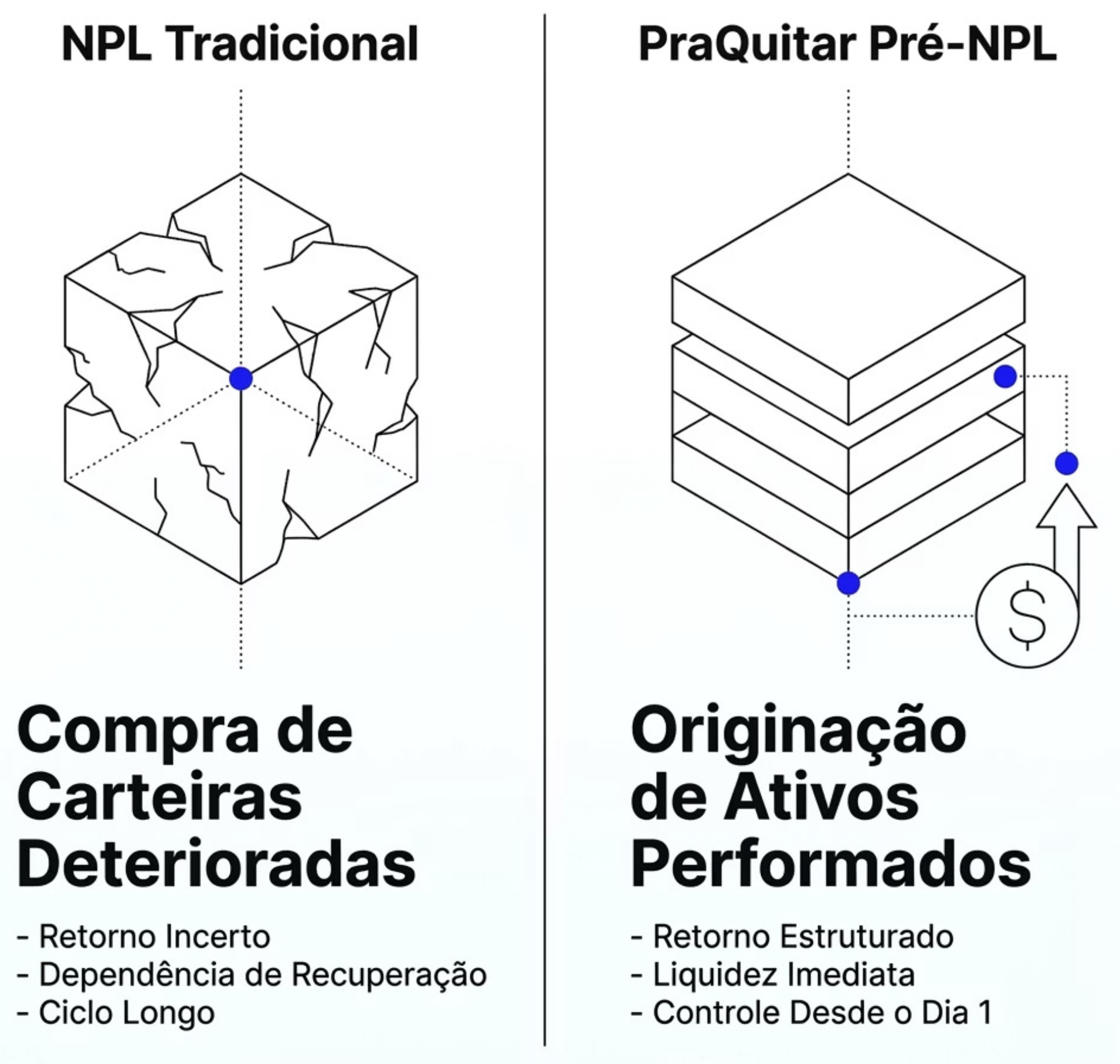

PraQuitar acts before the debt fully deteriorates — at the point of greatest economic efficiency.

- Before NPL

- Before value impairment

- Before structural inefficiency

The market buys the problem later.

PraQuitar captures value earlier.

The PraQuitar mechanism

Immediate liquidity, without a discount

New assets are generated in what we call Pre-NPL — when the creditor needs immediate liquidity but does not want to sell its portfolio at a discount. By settling the obligation on the debtor's behalf, the creditor eliminates collection costs, negative reporting, and default risk.

Upfront settlement and restored credit

We settle the obligation upfront with the creditor through a new structured loan to the debtor, even when no one else is willing to extend credit. The debtor immediately regularizes their situation, improves their credit score, and regains access to credit.

The debtor joins the solution

They access the proposal and accept the terms of the installment settlement.

Down payment and agreement

The debtor formalizes participation with a down payment and signs the new agreement.

PraQuitar settles with the creditor

The creditor receives the amount upfront. The original debt ceases to exist.

A new performing asset emerges

A new agreement is created — healthy, structured, and with predictable cash flow.

The debtor replaces an unstructured liability with a predictable obligation.

A natural evolution of the credit and collections market.

Debt ceases to be a problem and becomes a new performing asset

Definitive settlement closes the past. From there, a new structured financial relationship begins.

The debt ceases to exist. The asset begins to exist.

Infrastructure, not intermediation

PraQuitar does not merely participate in the system. It redefines the system.

A unique position in the credit market

While traditional NPL operates with compressed margins and long recovery cycles, PraQuitar acts before deterioration — originating performing assets from day one.

- Operationally validated model

- Funding and structure ready to scale

- First-mover advantage entry window

- Exposure to a segment with no institutional competition yet

The engine for scale

This new origination model enables funds to invest in a new credit pipeline with greater social and economic impact, advancing the evolution of Brazil's credit and collections system.

Impact at scale

PraQuitar transforms delinquency into structured credit origination.

Secure, regulated infrastructure

CORBAN model

A well-established regulatory structure in the financial market.

QI Tech infrastructure

State-of-the-art banking technology as the operational backbone.

Central Bank regulation

Operations compliant with BACEN regulations.

Validated legal structure

A legal model reviewed and approved for all parties.

Institutional-grade security for all parties.

The new infrastructure for Brazilian credit

PraQuitar does not improve the current model. It creates a new one.

The 3rd way is already here.

"We settle the past. We structure the future."

In the media

Press

Read coverage of PraQuitar and the impact of settlement on the credit market.

Schedule a meeting

Talk to a PraQuitar advisor

Complete the form and our advisor will contact you to schedule a meeting.